Private Equity

Apr 2, 2026

Permanent Capital Meets Private Markets

We analyse the transformative impact of life insurance platform integration on the business models, financial profiles, and market valuations of prominent alternative asset managers (AAMs). Relying on episodic fundraising through closed-end funds has long defined the growth and operating model of alternative asset managers (AAMs). Many firms have depended on periodic capital commitments from institutional investors, which, while effective for scaling private equity and credit strategies, expose ...

Mar 25, 2022

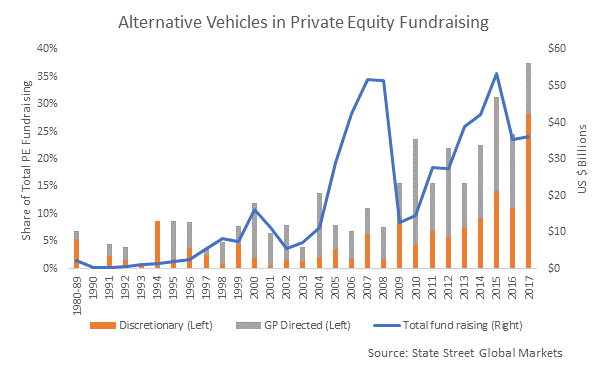

Investing Outside the Box: Evidence from Alternative Vehicles in Private Equity

By Josh Lerner, Jason Mao, Antionette Schoar, and Nan R. Zhang Published in the Journal of Financial Economics, January 2022. Contrary to common belief, returns in alternative vehicles in private equity increasingly depend on the match between GPs and LPs and both parties’ outside options. Using previously unexplored custodial data, we examine alternative investment vehicles (AVs) in private equity (PE) funds over the last four decades. By 2017, AVs reached 40% of all PE commitments. Average ...

Jan 29, 2021

Private Equity and the Leverage Myth

By Megan Czasonis, William Kinlaw, Mark Kritzman, and David Turkington. Published in the Journal of Alternative Investments, Winter 2021. Conventional wisdom regarding the way leverage affects volatility is incorrectly leading private equity investors to dramatically overestimate risk. A fundamental precept of corporate finance is that the volatility of a firm's equity is positively related to its leverage with one-to-one correspondence. Following this logic, investors commonly estimate the ...

Jun 1, 2019

Private Equity Valuations and Public Equity Performance

By Megan Czasonis, Mark Kritzman, and David Turkington Published in the Journal of Alternative Investments, Summer 2019 We find persuasive evidence that private equity managers produce positively biased valuations that appear to be rationalized by information that should not be relevant.

Mar 1, 2019

Private Equity Program Breadth and Strategic Asset Allocation

By Alexander Rudin, Jason Mao, Nan R. Zhang, and Anne-Marie Fink. Published in the Journal of Private Equity, Spring 2019. We create a custom “synthetic” peer group for each private equity program that mirrors the program’s strategy mix and number of fund commitments actually made each year. Our enhanced methodology corrects for the program breadth bias and creates a fairer process for assessing a program manager’s skill.

Jan 1, 2019

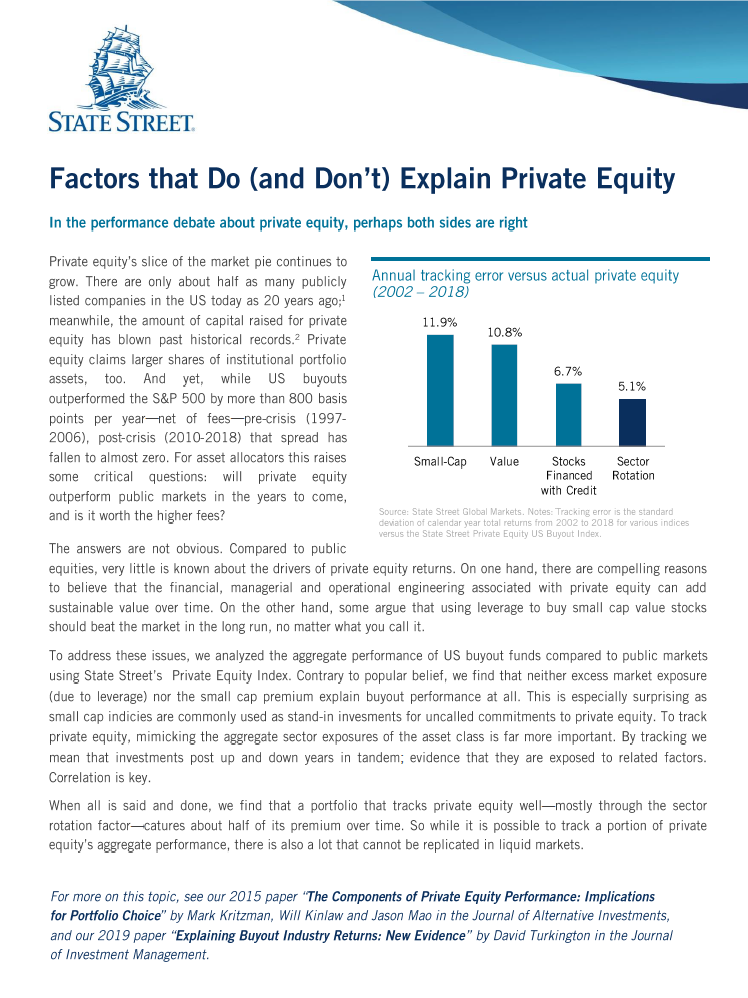

Explaining Buyout Industry Returns: New Evidence

By David Turkington Published in the Journal of Investment Management, First Quarter 2019. Contrary to popular belief, levered small cap value stocks do not actually track private equity returns, but other factors such as sector exposure do. As an asset class, private equity buyouts have outperformed the S&P 500 historically, but people disagree on why. One explanation is skill in picking and managing companies; another is that private equity loads up on “factors” like small cap value which ...

Sep 1, 2015

The Components of Private Equity Performance: Implications for Portfolio Choice

By Will Kinlaw, Mark Kritzman, and Jason Mao. Published in the Journal of Alternative Investments, Fall 2015. We use a proprietary database of private equity returns to measure the excess return of private equity over public equity and to partition this return into two components: an asset class alpha and compensation for illiquidity.

Sep 1, 2014

The Divergence of High- and Low-Frequency Estimation: Causes and Consequences

By William Kinlaw, Mark Kritzman, and David Turkington Published in the Journal of Portfolio Management, 40th Year Special Anniversary Issue and recipient of the 2014 Bernstein Fabozzi/Jacobs Levy Outstanding Article Award. Financial analysts are often surprised by the extent to which assets that are thought to be strongly correlated diverge over time. We analyze the causes and consequences of the divergence of high- and low-frequency estimation, and we present a framework for constructing portfolios ...

Dec 1, 2013

Liquidity and Portfolio Choice: A Unified Approach

By William Kinlaw, Mark Kritzman, and David Turkington. Published in the Journal of Portfolio Management, Winter 2013. Our research on “Liquidity and Portfolio Choice” provides a framework for asset owners to evaluate the benefits of liquidity and costs of illiquidity, and implications for strategic asset allocation. READ THE 1-PAGE SUMMARY

Dec 1, 2013

Liquidity and Portfolio Choice: A Unified Approach

By William Kinlaw, Mark Kritzman, and David Turkington. Published in the Journal of Portfolio Management, Winter 2013. Our research on “Liquidity and Portfolio Choice” provides a framework for asset owners to evaluate the benefits of liquidity and costs of illiquidity, and implications for strategic asset allocation. READ THE 1-PAGE SUMMARY

1. Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010. Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012, 2021, 2023. Harry M. Markowitz Award for Best Paper in the Journal of Investment Management in 2022, 2023. Doriot Award for Best Private Equity Research Paper in 2022.