The Stock Bond Correlation

By Megan Czasonis, Mark Kritzman, David Turkington, State Street Associates

Feb 1, 2021

By Megan Czasonis, Mark Kritzman, and David Turkington.

Published in the Journal of Portfolio Management, February 2021.

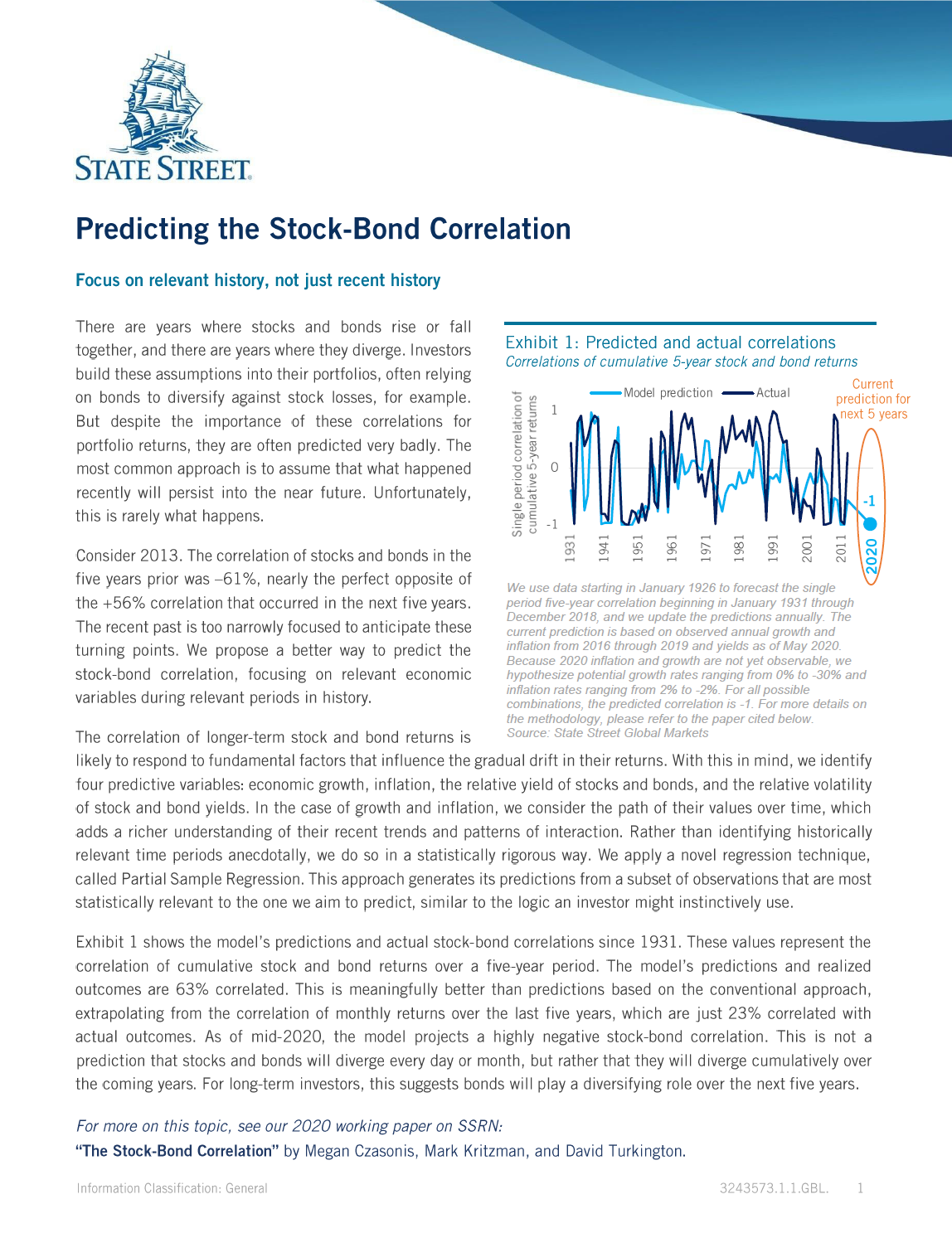

We propose a more reliable way to predict the stock-bond correlation, focusing on relevant economic variables during relevant periods in history.

1.Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Doriot Award for Best Private Equity Research Paper in 2022; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012 and 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010.