The Fallacy of Concentration

By Mark Kritzman, and David Turkington

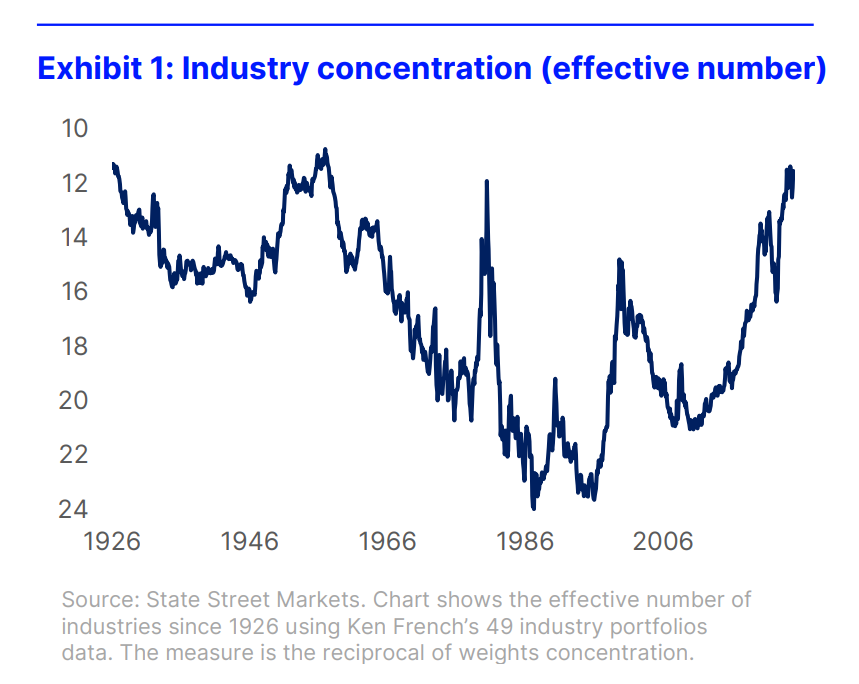

Evidence shows that concentrated market capitalization weights do not make an index riskier, because larger stocks are inherently more diversified and their increased weights are offset by their lower volatility compared to small stocks.

The dominance of large tech firms in market-cap-weighted indices has sparked recent concern about concentration risk, but historical data and empirical analysis suggest these fears may be unfounded. A review of nearly 90 years of market performance shows that reducing exposure based on concentration offers no timing advantage and actually worsened returns and risk. Sector-level concentration also fails to distinguish between high and low risk or strong and weak performance. Moreover, large companies tend to be safer due to their more diversified operational footprint and the increased investor and regulatory scrutiny they receive. Ultimately, the presence of concentrated capitalization weights has not proven to be a reliable indicator of bubbles or future market downturns.