September 26, 2025

What to Watch

Complimentary CONTENT

What to watch test

September 26, 2025

By: Alberto Cavallo, Alex Cheema-Fox

- Alberto CavalloPartner State Street Associates

- Alex Cheema-Fox, CFAManaging Director, Investor Behavior Research

1. US Treasury 10-year yield is a single factor model

Those hoping that a revival of term premium would increase Treasury yields are forced to face the cold hard fact.s Term premium remains depressed and not terrible volatile. The key driver of US Treasury 10-year yields remains rate expectations in recent months.

As recently as April, the size of Fed Fund rate cuts priced for Jan-25 was 34 bps, which was consistent with a UST-10y of 4.70. Ahead of NFP release the strip discounts of 107bps of rate cuts and the US Treasury yield is 3.94%

2. Does a steeper U.S. yield curve signal recession?

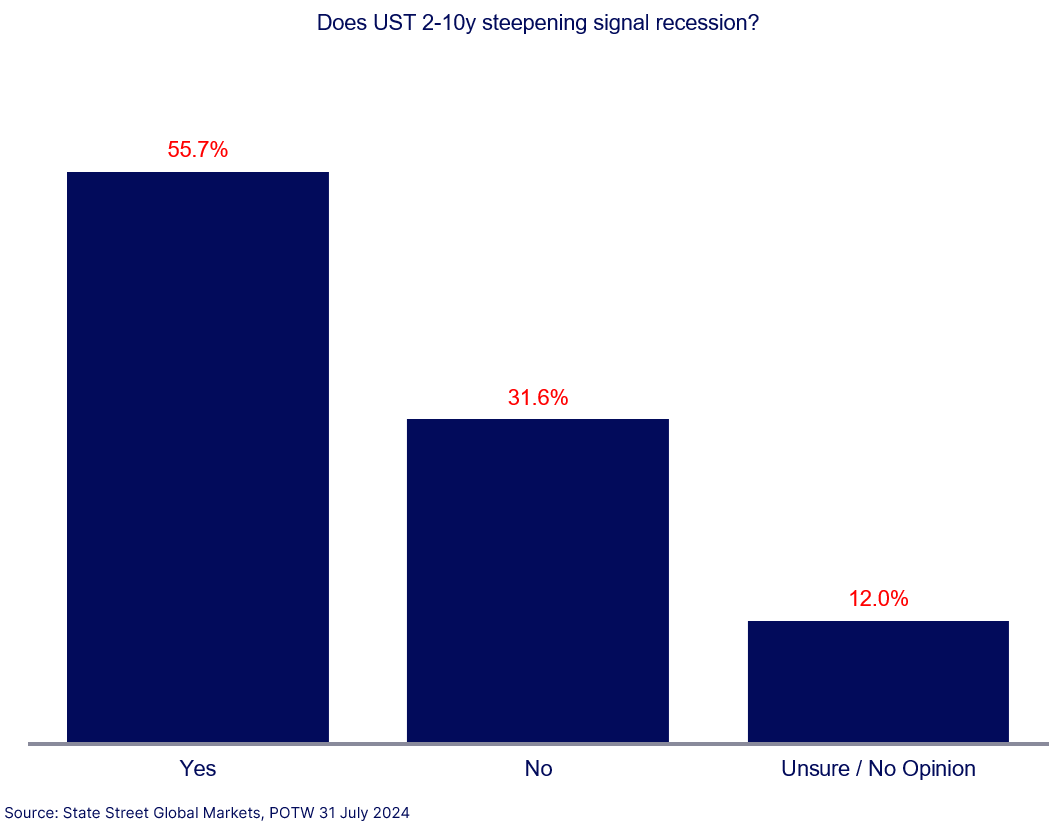

The US Treasury 2-10y yield curve has bull steepened. At the end of June, it was near -50bps inverted, compared to the current (pre-NFP) reading of -19bps. Historically, steepening from an inverted level has been a reliable indicator of recession is coming in short order.

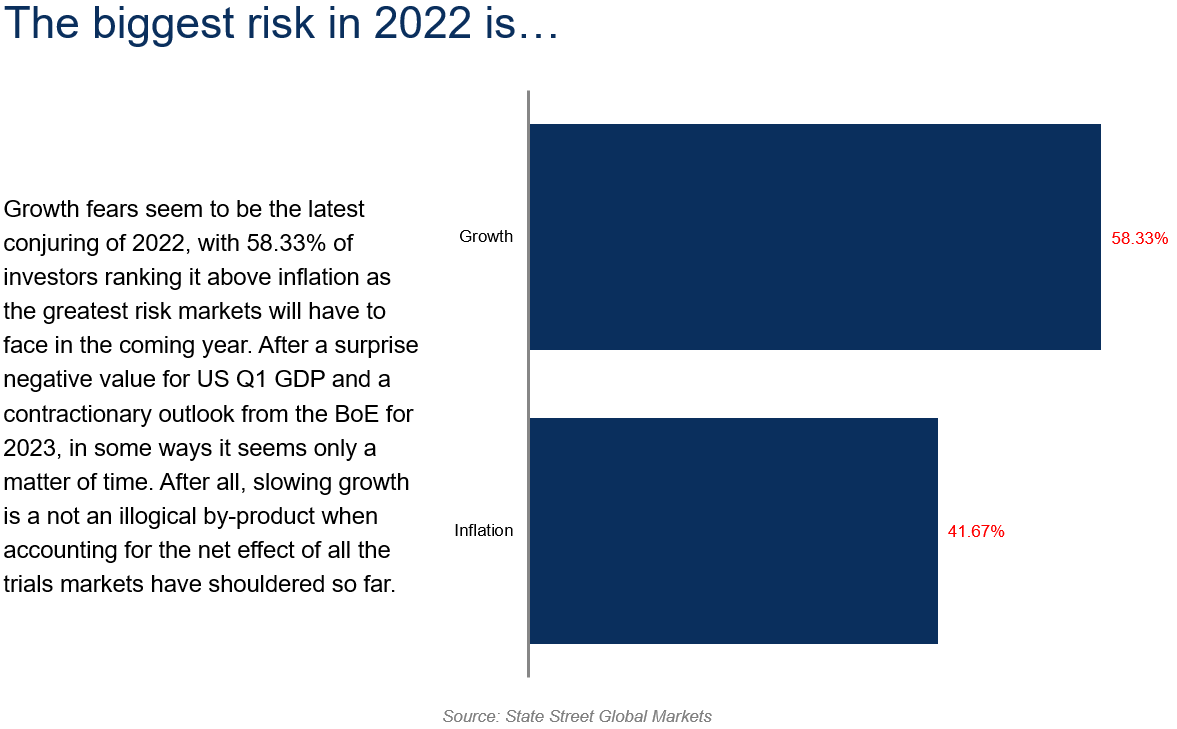

More than half of respondents worry that this might be the case. The result is interesting to the extent that the belief in the soft landing has become rather more prevalent over the past year. Are opinions changing now?

3. Looking Recessionary

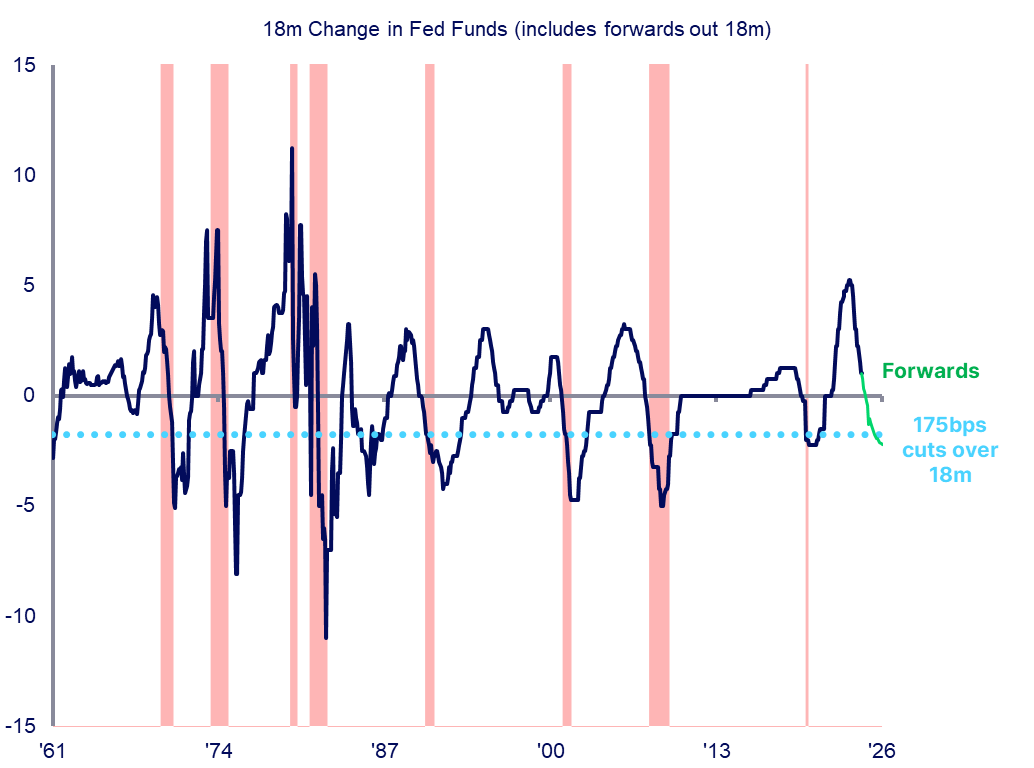

A chart from Deutsche Bank’s economics team caught our eye. They graph the 18-month change in Fed Funds. The series is extended in the future by using the Fed Funds futures.

When the 18-month change shows cuts of 175bps or larger, this has corresponded with a recession. Although it is fair to say that those holding the soft-landing view outnumber those worried about recession, this chart is certainly food for thought.

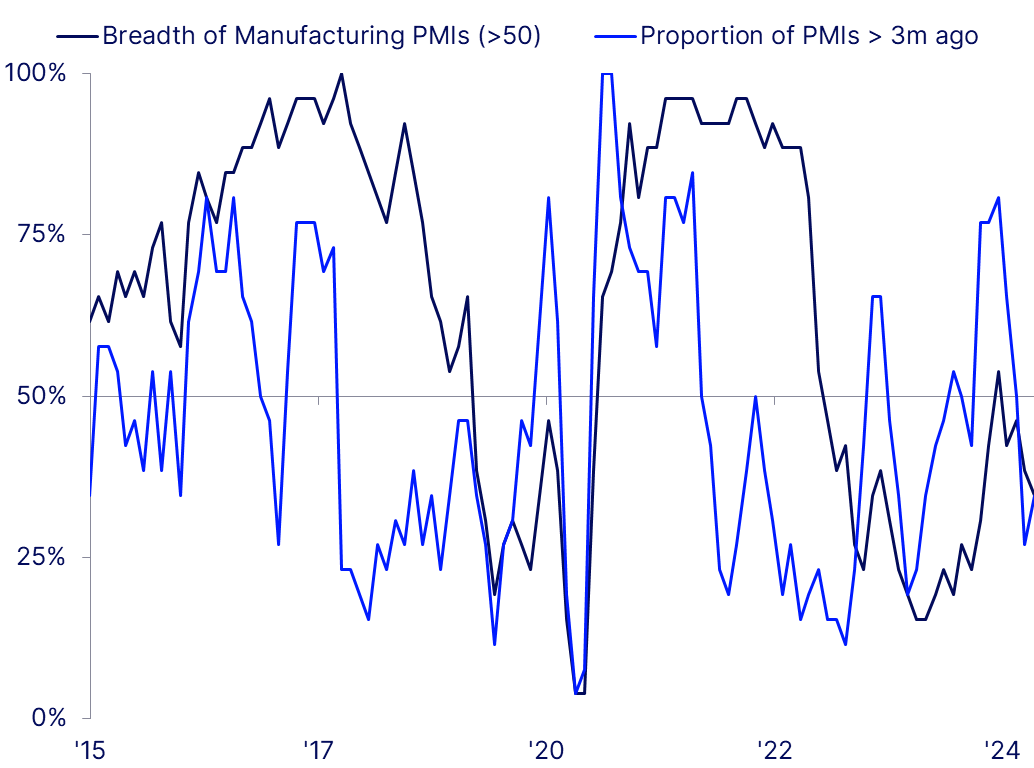

4. The rates outlook is more than an inflation story

The global interest rate easing cycle is frequently considered in the context of inflation. However, this often masks challenges in real economic activity, particularly a weaker manufacturing sector.

Cross-country PMIs shows this trend clearly. The breadth of Manufacturing PMIs calculates the proportion of 26 countries that report above 50 level PMI’s: this has fallen to around a third. This coincides with a similar proportion of countries reporting PMI levels higher than three months ago. The trend of softer inflation supports rate easing largely discounted across global rates markets; weaker economic conditions add another flip of support to rate pricing.

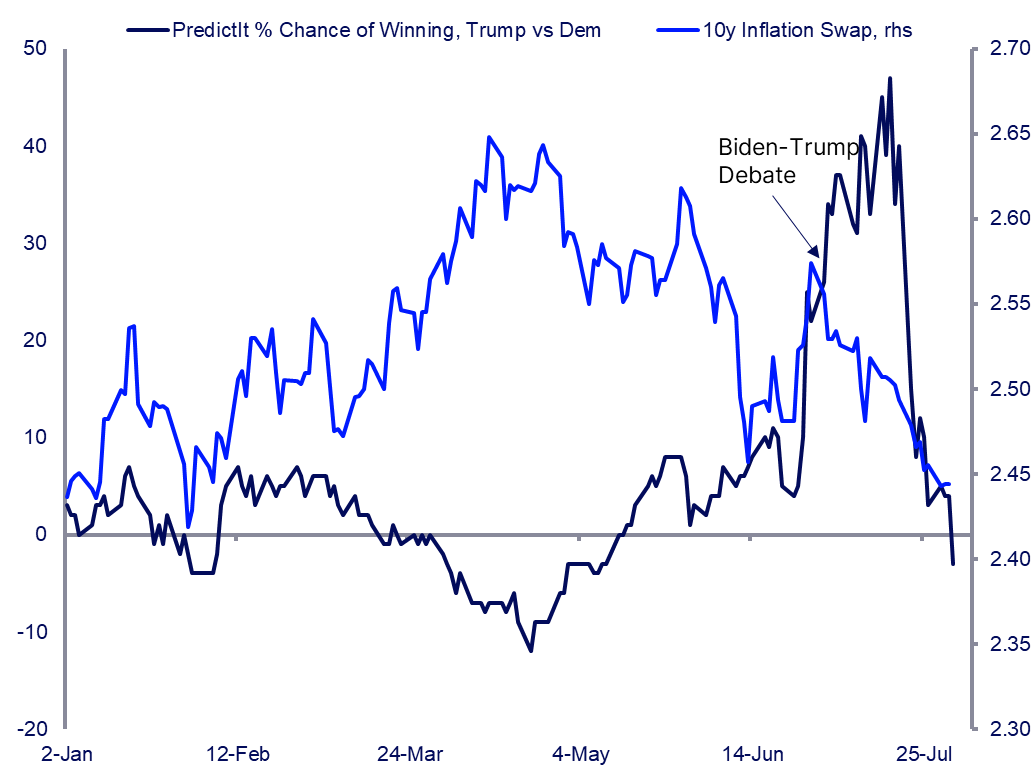

5. A Trump Trade falls on hard times

Rising inflation expectations are one of the commonly forecasted outcomes of a second Trump presidency, particularly when both houses of Congress were also seen within the Republicans’ grasp. They jumped following President Biden’s poor debate performance in late June, an event that ultimately catalysed his departure from the race.

But the rise was fleeting, even when Biden was still a viable candidate and as Trump’s probability of victory kept growing. Now, with VP Harris’ entry into the race, polls narrowing, the race a toss-up and a GOP sweep looking far less likely, inflation expectations are back to the lows of the year.

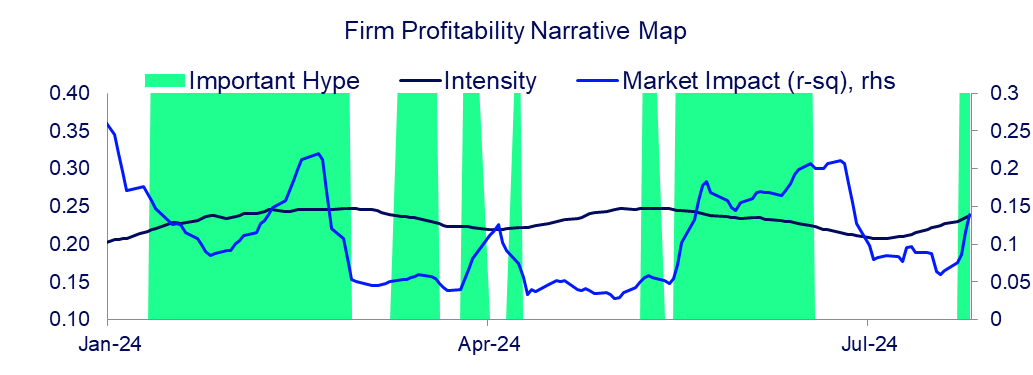

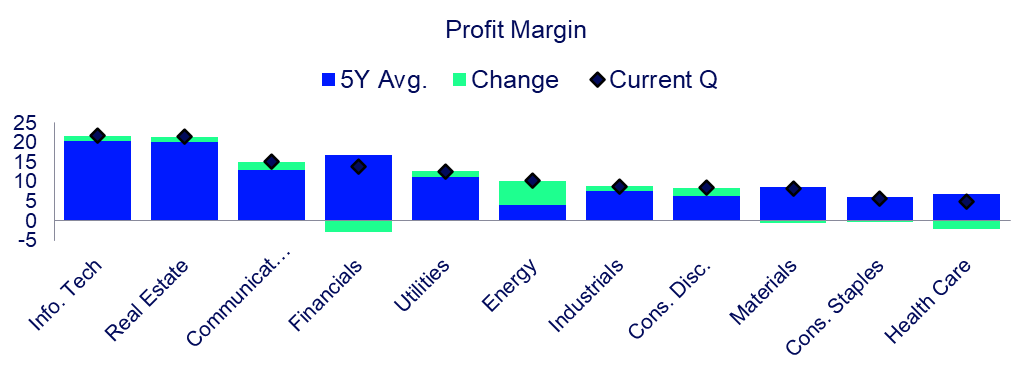

6. Patience is a virtue

Tech has caught a stray bullet from the media as talks of firm profitability has gained intensity. As we break into the heart of Q2 earnings, investors’ perception of profitability has had an increasing impact on the market. Areas of tech, specifically Semis and Software, are being punished by this narrative as investors are becoming impatient waiting to see AI churn a significant profit. Tech companies are allocating an increasing amount of CapEx towards AI, but the profit isn’t being reflected in earnings. This impatience seems to be more of a market overreaction rather than an actual profitability issue. In reality, tech profits are some of the best in the market as they are currently higher than the 5-year average and continuing to grow.

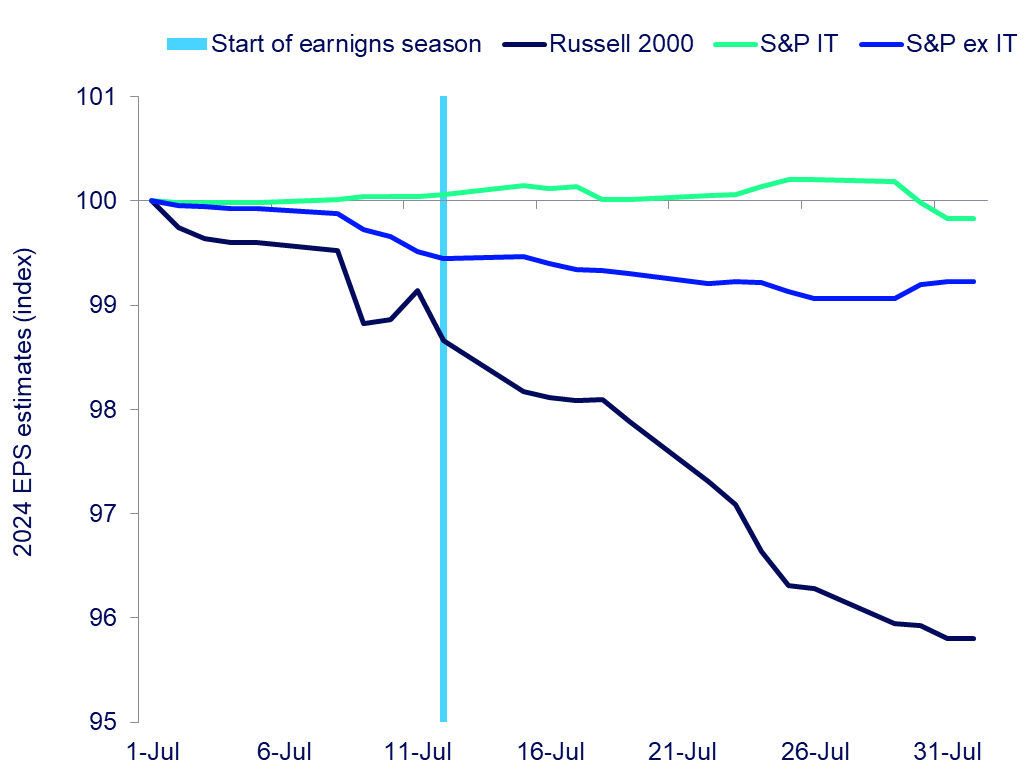

7. Earnings look to weaken … particularly in small caps

Market’s assessment of Tech earnings as “disappointing” seems excessively harsh. It was not impressed by Alphabet beating by only a small margin, or Microsoft’s cloud business growing by 29% instead of 31% expected. Perhaps huge positions in IT are to blame.

To us the bigger disappointment from the earnings season is consistent earnings. Those are, ironically, concentrated outside IT sector and mostly in Small Caps. We find those stocks particularly at risk once excessive positions in IT are washed out.

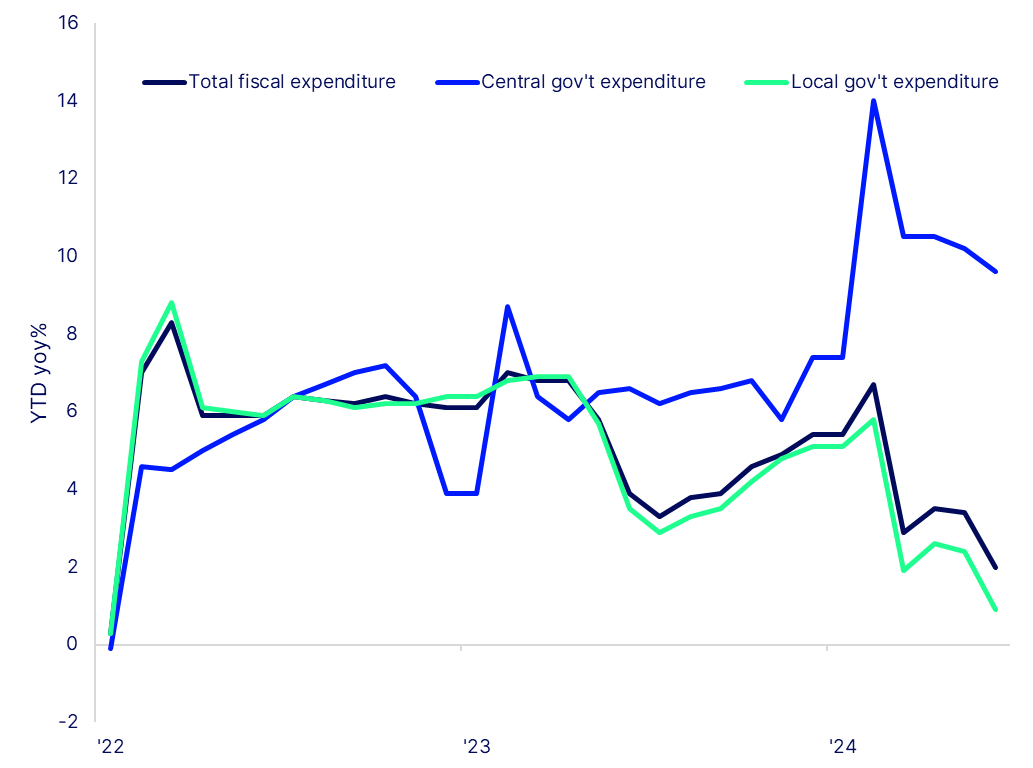

8. More Fiscal Firepower to Come

After rolling out rate cuts last week, Beijing took another step this week to signal more fiscal support to boost economic recovery. The July Politburo meeting that ended on Tuesday and MoF official press conference called for more proactive fiscal policy and underscored the need for the country to accelerate the issuance of local government special bonds and ensure effective usage of both ultra-long special sovereign bonds and local government special bonds to invest in infrastructure and new industries.

So far in 2024, government spending has been slow, weighed down by local government that faces elevated debt levels as well as increasing debt costs. Central government on the other hand, has more policy room to pick up the slack, and will likely continue to do so in 2H of the year.

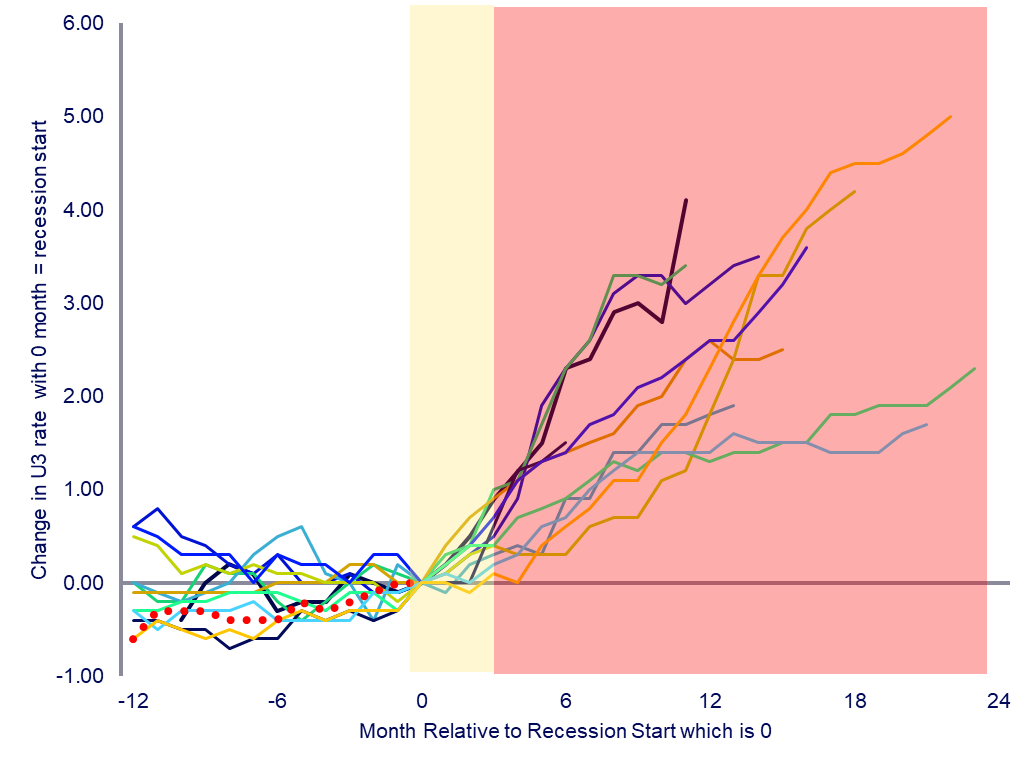

9. Unemployment and Recessions

There is much discussion about how fast the unemployment rate (U3) may increase. One factor that will determine its rise include immigration policies, which are dependent on the U.S. Presidential election. Another factor is related to demand and whether non-linearity kicks in.

The chart shows the change from the first month of recession (1948 to present) but does not include the pandemic. Typically, in the first couple of months of a recession, U3 increases slowly, and then later it accelerates.

10.Machine learning brings exciting opportunities to investing

Machine learning brings exciting opportunities to investing

Disclaimer & Risk

Author Bios

Alberto Cavallo

Alberto Cavallo is the Thomas S. Murphy Professor of Business Administration at Harvard Business School, where he teaches in the Business, Government, and the International Economy (BGIE) unit, a Faculty Research Fellow at the National Bureau of Economic Research, and a member of the Technical Advisory Committee of the US Bureau of Labor Statistics (BLS). Professor Cavallo's research focuses on the behavior of prices and its implications for macroeconomic measurement and policies. His work is based on the use of daily data collected from hundreds of online retailers around the world. He co-founded The Billion Prices Project, an academic initiative at MIT and Harvard University that pioneered the use of online data to conduct research on high-frequency price dynamics and inflation measurement.

Alex Cheema-Fox

Alex Cheema-Fox leads Multi-Asset Research in the Quantitative Markets Research Group at State Street Associates (SSA), focusing on investor behavior. Since joining SSA in late 2008, Alex has contributed to the construction and application of behavioral measures spanning the fixed-income, equity, factor and foreign exchange spaces. He has presented this research globally at numerous conferences. Prior to joining SSA, Alex worked at the RIS Consulting Group, where he built and applied quantitative risk models for customized structured products, serving a variety of institutional clients including asset owners and asset managers. Alex holds a bachelor's degree in mathematics, a master's degree in quantitative finance, a master's degree in computer science, the FRM certification and the CFA charter.

The information provided herein is not intended to suggest or recommend any investment or investment strategy, does not constitute investment advice, does not constitute investment research and is not a solicitation to buy or sell securities. It does not take into account any investor's particular investment objectives, strategies or tax status. Past performance is no guarantee of future results. For more information, please see the link for the marketing disclaimer for State Street Markets research, available in the “Legal Disclosure” section of our “Disclosures” page referenced in the footer below.

- © State Street Corporation

- Privacy Notice

- Legal Disclosure

- Product-Specific Disclosure

1.Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Doriot Award for Best Private Equity Research Paper in 2022; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012 and 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010.